The programme was developed in conjunction with the Association of Short-Term Lenders (ASTL) and Financial Intermediaries and Brokers Association (FIBA). It is designed to build skills and knowledge of the specialist property finance sector, including bridging finance, buy to let lending, commercial mortgage lending, and development finance. Key Skills Include: Ability to apply understanding and identify most suitable product for customers Understanding of exit strategies of financial products Understanding of regulatory and processing requirements, and how each of them is underwritten Understanding of the benefits and risks of different specialist finance products, to customers and lenders Understanding of the different types of specialist property finance options.

We were able to provide a commercial mortgage to a North Yorkshire landlord who had previously taken a two year bridging loan to secure the purchase of a pub. The landlord was a new entrant to the leisure industry two years ago, having retired from his previous profession 12 months earlier. Therefore, The client had less than the 3 years of minimum experience required by commercial mortgage lenders operating in this sector at the time. On this basis Equinox Commercial Finance were able to provide a 2 year Commercial Bridging Loan to the client, which enabled him to purchase the property. At the end of the 2 year term the client had enough experience to be able to re-finance onto a long-term commercial mortgage, although given the current climate most lenders had withdrawn their appetite to lend to the sector. The client had implemented some impressive growth plans including increasing the size of the rear bar area, further decorative improvements and development of the outside areas. He had also made significant cost reductions, which helped his cash flow position. On this basis Equinox Commercial Finance were able to provide a mid term Commercial Mortgage product to the client, with a view to refinancing again when the current turbulence in the lending market subsides and mainstream lenders are open to the leisure sector once again.

We were approached by a local accountancy practice who were looking to refinance property within its existing SSAS Pension Fund to purchase a new office. The client was looking to raise capital of £330k to complete the purchase. Equinox Commercial Finance were able to place the client with a specialist lender that was able to offer 55% LTV over 25 years at 5.85% + BOE Base Rate.

We were approached by a UK ex-pat currently living in Canada who wished to refinance a commercial investment mortgage to buy more property. The client was looking for the maximum loan to value (LTV) available on his personally owned portfolio of three fully tenanted industrial units located in Surrey, valued at £1.15 million. The limiting factor for the client was his current ex-pat status, which precluded him from offers of funding from all of the mainstream high street banks. Equinox Commercial Finance were able to place the client with a specialist lender that was able to offer 60% LTV and a 5-year fixed rate.

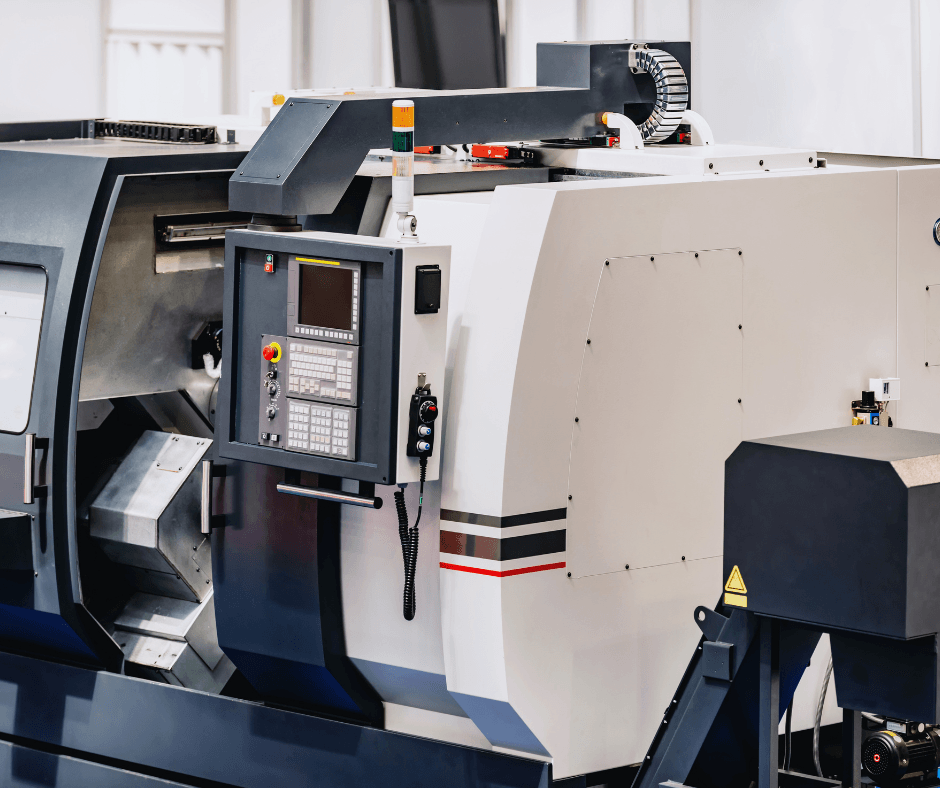

We were approached by a local business wishing to purchase a CNC Machine to improve the output and efficiency of their busy production line. A CNC machine would allow for the automation and control of machine tools and can be used to perform precise cuts and other machining tasks, that would be difficult to do with the human hand. CNC machines are also used on tasks that humans can do themselves, but which would take them much longer to complete. We have access to a whole of market panel of lenders and were able to quickly secure hire purchase finance for the machine at a competitive rate of 5.3% over a 7-year term.

The start of 2022 saw a jump in new tenants looking to rent UK commercial property, with the uplift particularly prevalent in prime office space. Investor enquiries across all UK commercial property also continued to rise, according to the RICS. Read the Full Report here>

The UK holiday let industry has been steadily growing in popularity among property investors and holiday goers alike and doesn’t look to be slowing down anytime soon! The yields available on holiday let properties have rocketed, and it is no surprise to see well-maintained properties, in the right locations, producing yields over 12% per annum. Holiday let properties offer some landlords an alternative tax-efficient investment vehicle, due to a more favourable treatment of loan interest. This has been felt even more by landlords since the full loan-interest tax-relief restrictions came into force in April 2020. However, we advise that clients seek professional tax advice before making any decisions. We have access to a wide pool of lenders offering holiday let mortgages. They typically offer: A maximum loan to value (LTV) of 75% Rates from 3.29% on a two-year fixed rate, through to 3.79% for a five-year fixed rate. Mortgages are available to individuals, property holding companies, or trading limited companies (i.e. the client's current business operation). If you are looking to diversify your property investment portfolio, or continuing to expand an existing holiday let portfolio please call us on 01845 591488.

We've recently seen an increase in enquiries from business owners looking to purchase property from which to run their company. Often, their existing landlord has offered to sell them the property before putting it on the open market. Others have found recently vacated property, which perfectly suits their businesses’ requirements. For example, we recently placed a relocating Children's Day Care Nursey client with a lender who was able to offer a mortgage equal to 65% of the full going concern value of the nursery, which included the goodwill of the business at an interest rate of 3.92%, fixed for 10 years. If purchasing your own business premises is something you’re looking to do, we can help.

The Recovery Loan Scheme (RLS) launched on 6 April 2021 to help UK businesses access finance as they recover and grow following the Covid-19 pandemic. The scheme aims to help businesses affected by coronavirus and can be used for business purposes, such as managing cash flow, investment and growth. A key aim of the scheme is to improve the terms on offer to businesses. Businesses who have taken out a Coronavirus Business Interruption Loan Scheme (CBILS), Coronavirus Large Business Interruption Loan Scheme (CLBILS) or Bounce Back Loan Scheme (BBLS) facility are able to access the new scheme. The scheme will run until 31 December 2021, subject to review. It is important to note that if you are approved for a Recovery loan, you will be liable to pay the RLS interest payments and fees from the outset. The guarantee is to the lender and not to the business. Am I eligible for a Recovery loan? To receive a loan under the Government’s Recovery Loan Scheme (RLS), you’ll need to meet the following criteria: Business has been impacted by coronavirus Minimum of 2 years’ trading history Must be a limited company or limited liability partnership (LLP) Business is trading in the UK Loan is for business purposes (i.e. working capital or investment, and to support trading in the UK) You Could Apply for a Recovery Loan to: Access cash flow Grow your business Purchase equipment Pay a one-off cost Help with payroll Invest in marketing Please call us on 01845 591488 to make an enquiry.

We were approached by a West Yorkshire operator of a Children's Day Care Nursery who wished to move to larger premises to accommodate her rapidly expanding classes. The client had achieved a strong recent financial performance, even over the pandemic, and had received excellent Ofsted reports. The target property was on the market for £230,000 and although the client was able to raise a 30% deposit for the purchase she needed to undertake minor refurbishment work to the premises. The client was renting her current property and this meant that she could add her rental payments back in to her profits to improve her debt serviceability. Equinox Commercial Finance were able to place this client with a major high street lender who was able to offer a mortgage equal to 65% of the full going concern value of the nursery, which included the goodwill of the business. This provided enough capital to purchase the new premises and undertake the required refurbishment work. Interest rate 3.92%, fixed for 10 years.